Nevertheless, mortgage-backed securities costs tend to increase at a reducing rate when bond rates are falling; in turn, their costs tend to reduce at an increasing rate when rates are rising. This is called unfavorable convexity and is one reason MBSs offer greater yields than U.S. the big short who took out mortgages. Treasuries. Mortgage-backed securities are often utilized to hedge the overall threat of a financier's fixed earnings portfolio due to negative convexity.

It needs to be noted that mortgage-backed securities tend to produce their best relative performance when dominating rates are stable. Home mortgage swimming pools can be produced by private entities (in the majority of cases) or by the 3 quasi-governmental companies that issue MBSs: Government National Home mortgage Association (referred to as GNMA or Ginnie Mae), Federal National Home Loan (FNMA or Fannie Mae), and Federal House Loan Home Mortgage Corp.

The most succinct description of the differences among the 3 originates from the U.S. Securities and Exchange Commission (SEC): "Ginnie Mae, backed by the complete faith and credit of the U.S. federal government, ensures that financiers get prompt payments. Fannie Mae and Freddie Mac likewise supply particular assurances and, while not backed by the full faith and credit of the U.S.

Treasury. Some personal institutions, such as brokerage companies, banks, and homebuilders, likewise securitize home mortgages, known as "private-label" mortgage securities." MBSs backed by Ginnie Mae aren't at threat of default, however there is a little degree of default threat for a bond issued by Fannie Mae and Freddie Mac. Still, Freddie and Fannie's bonds have a stronger component of support than they appear to because both were taken control of by the federal government in the wake of the 2008 monetary crisis.

Many investors who own a broad-based bond mutual fund or exchange-traded fund have some exposure to this sector considering that it is such a large portion of the markettherefore it is one that is greatly represented in varied funds. Financiers can also choose for funds that are dedicated solely to MBSs.

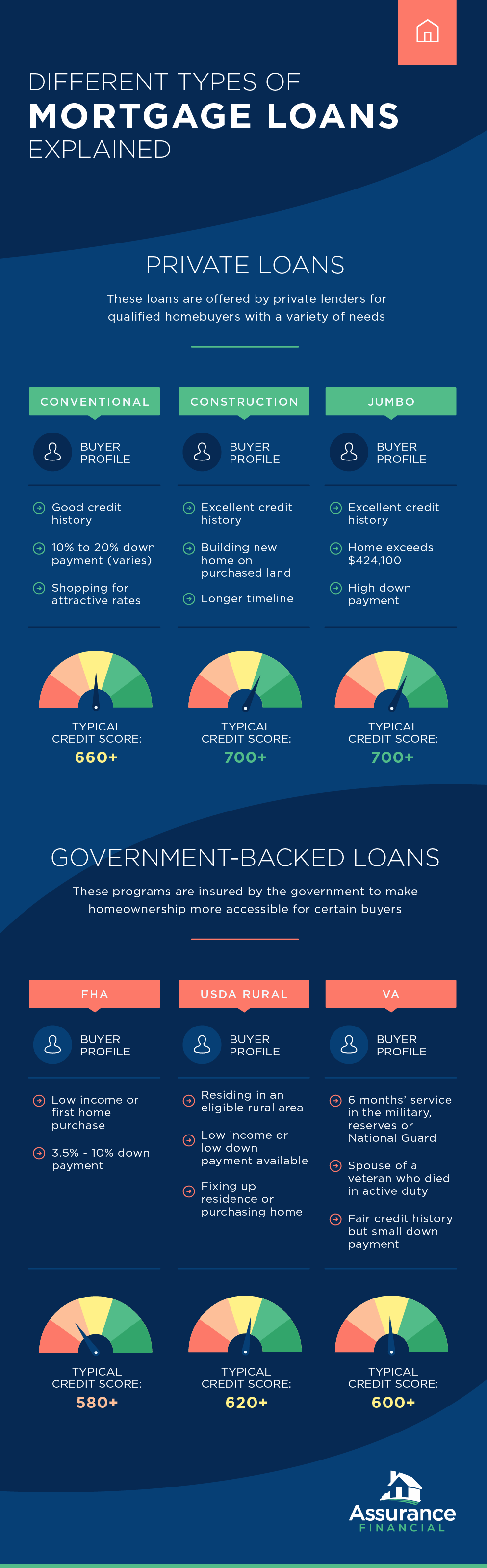

Little Known Questions About What Are Brea Loans In Mortgages.

Our ideas at California Pools & Landscape are with everyone who has actually been affected by the Coronavirus. Our clients and workers are our primary top priority and as such, we are adjusting to preserve our high quality of service in the safest possible method. Here is how we have adjusted our operations to more securely meet the requirements of our customers: Online meetings with designers.

Appropriate operation, upkeep, and disinfection (e. g., with chlorine and bromine) of swimming pools and jacuzzis ought to get rid of or inactivate the virus that triggers COVID-19.

A Mortgage-backed Security (MBS) is a financial obligation security that is collateralized by a mortgage or a collection of home mortgages - how did clinton allow blacks to get mortgages easier. An MBS is an asset-backed security that is traded on the secondary marketOption Investment Market (GOAL), which allows financiers to benefit from the home mortgage service without the need to directly buy or offer home mortgage.

A home mortgage included in an MBS should have originated from an authorized monetary institution. When an investor buys a mortgage-backed security, he is basically providing cash to home buyers. In return, the investor gets the rights to the value of the home mortgage, consisting of interest and primary payments made by the debtor.

The bank serves as the middleman between MBS financiers and house buyers. Normal buyers of MBS consist of private financiers, corporationsCorporation, and institutional financiers. There are 2 standard kinds of mortgage-backed security: and. The pass-through mortgage-backed security is the easiest MBS, structured as a trust, so that principal and interests payments are travelled through to the financiers.

What Is Minimum Ltv For Hecm Mortgages? - Truths

The trust that sells pass-through MBS is taxed under the grantor trust rules, which determines that the holders of the pass-through certificates need to be taxed as the direct owners of the trust apportioned to the certificate. Collateralized home mortgage obligations consist of numerous swimming pools of securities, likewise understood as tranches. Each tranche features various maturities and top priorities in the receipt of the principal and the interest.

The least dangerous tranches provide the least expensive rates of interest while the riskier tranches come with greater rate of interest and, thus, are usually more chosen by investors. When you want to purchase a home, you approach a bank to offer you a home loan. If the bank confirms that you are creditworthy, it will transfer the cash into your account.

The bank may pick to collect the principal and interest payments, or it may opt to offer the mortgage to another banks. If the bank chooses to sell the home mortgage to another bank, government institution, or private entity, it will use the earnings from the sale to make brand-new loans.

It then sells these mortgage-backed securities to interested financiers. It uses the funds from the sale to purchase more securities and drift more MBS outdoors market. As a response to the Great Depression of the 1930s, the government established the Federal Housing Administration (FHA) to help in the rehabilitation and building of property houses.

In 1938, the federal government developed Fannie Mae, a government-sponsored firm, to purchase the FHA-insured home mortgages. Fannie Mae was later split into Fannie Mae and Ginnie Mae to support the FHA-insured mortgages, Veterans Administration, and Farmers House Administration-insured mortgages., In 1970, the federal You can find out more government developed another company, Freddie Mac to carry out comparable functions to those performed by Fannie Mae.

The Definitive Guide for How lake powell houseboat timeshare Do Reverse Mortgages Work When You Die

They likewise ensure timely payments of principal and interest on these mortgage-backed securities. Even if the initial borrowers fail to make timely payments, both institutions still pay to their investors. The government, nevertheless, does not guarantee Freddie Mac and Fannie Mae. If they default, the federal government is not bound to come to their rescue.

Unlike the other two firms, Ginnie Mae does not acquire MBS. Therefore, it includes the lowest risk amongst the 3 agencies. Low-grade mortgage-backed securities were amongst the elements that resulted in the monetary crisis of 2008. Although the federal government controlled the banks that developed MBS, there were no laws to straight govern MBS themselves.

If the customers of home mortgage loans defaulted, there was no sure method to compensate MBS investors. The market attracted all kinds of home loan lenders, consisting of non-bank monetary institutions. Standard lenders were forced to decrease their credit standards to complete for mortgage business. At the exact same time, the U.S. federal https://jaidenaknf178.weebly.com/blog/the-how-to-hold-a-pool-of-mortgages-statements government was pressing loan provider to extend home mortgage funding to higher credit threat customers.

Numerous debtors simply entered mortgages that they eventually might not afford. With a stable supply of, and increasing need for, mortgage-backed securities, Freddie Mac and Fannie Mae aggressively supported the marketplace by issuing more and more MBS. The MBS developed were increasingly low-grade, high-risk financial investments. When mortgage debtors began to default on their commitments, it caused a cause and effect of collapsing MBS that eventually cleaned out trillions of dollars from the United States economy - who provides most mortgages in 42211.

We hope you delighted in reading CFI's guide to a mortgage-backed security. CFI uses the Financial Modeling & Evaluation Analyst (FMVA)FMVA Accreditation certification program for those looking to take their professions to the next level. To keep learning and advancing your profession, the following resources will be useful:.